Originally published: June 2026

A probate appraisal in Illinois is a licensed appraiser’s written determination of a property’s fair market value as of the exact date the owner died.

Illinois executors must order this valuation after receiving letters of office, before filing the estate inventory, and before distributing any assets to beneficiaries.

A missing or defective appraisal freezes the estate, exposes the executor to personal liability, and can trigger IRS penalties on estates subject to Form 706.

A probate appraisal is a licensed appraiser’s formal written determination of a property’s fair market value as of the date the property owner died. Under 755 ILCS 5/ Article XIV, Section 14-2, the estate representative may employ one or more competent, disinterested appraisers and pay each of them reasonable compensation for their services.

The appraiser physically inspects the property, analyzes comparable sales that closed on or before the date of death, and produces a written report that satisfies both Illinois probate court standards and IRS documentation requirements.

A probate appraisal differs from a standard residential real estate appraisal in one critical way: the effective date is fixed in the past. The appraiser does not value the property as it sits today.

The appraiser reconstructs what the property was worth on the day the owner died — even if that date was 12 or 18 months ago. This backward-looking analysis is called a retrospective appraisal, and it requires documented research into historical market conditions rather than current listings.

A probate appraisal also differs from a broker price opinion, a comparative market analysis, or an automated online estimate. Illinois courts and the IRS do not accept those substitutes as valid documentation of estate value.

Executors who rely on informal valuations risk inventory rejections, beneficiary challenges, and personal liability if the estate is later audited. Understanding the role of a real estate appraiser in the probate process helps executors avoid those outcomes before they become costly.

| Valuation Type | Who Prepares It | Accepted by IL Probate Court | Accepted for IRS Form 706 |

| Licensed appraisal (USPAP-compliant) | Certified residential or commercial appraiser | Yes | Yes |

| Broker price opinion (BPO) | Licensed real estate agent | Generally no | No |

| Automated valuation model (AVM) | Algorithm (Zillow, Redfin, etc.) | No | No |

| Comparative market analysis (CMA) | Real estate agent | Generally no | No |

Probate deadlines move fast, and one missed appraisal can freeze the entire estate. Schedule your estate appraisal with Whitsitt & Associates today and keep Champaign County probate on track.

Illinois probate requires a real estate appraisal whenever the decedent owned real property solely in their own name that must pass through the probate estate. Under 755 ILCS 5/ Article IX, Section 9-8, a formal probate proceeding is generally necessary when the deceased person owned assets solely — not jointly — and all probate assets together exceed $150,000 in 2026.

Any estate that meets that threshold and includes real property requires a licensed appraisal as part of the formal estate inventory.

The inventory is the executor’s sworn accounting of every estate asset and its value as of the date of death.

Real estate almost always requires a professional estate settlement appraisal because property values are not self-evident, fluctuate after the date of death, and become a flashpoint for beneficiary disputes when heirs receive unequal shares.

Illinois probate courts treat the appraisal as the authoritative valuation baseline for all real property in the inventory.

Once the court issues letters of office appointing the executor, the appraisal process begins. The executor must complete the inventory before paying estate debts, distributing assets, or filing a final accounting.

Executors who delay the appraisal order routinely find themselves stalled at every subsequent step of administration. Ordering the appraisal within the first thirty to sixty days after appointment keeps the entire probate appraisal process on schedule.

Real property held in a living revocable trust, titled in joint tenancy with right of survivorship, or subject to an Illinois transfer-on-death deed, passes outside of probate and does not require a court appraisal.

That said, a date-of-death appraisal for those assets may still be necessary for tax assessment purposes or to document the stepped-up basis that beneficiaries carry forward.

A date-of-death valuation is a retrospective appraisal that establishes the fair market value of a property on the exact day the owner died. The date is fixed by law and cannot be adjusted by the executor, the appraiser, or the probate court, regardless of how much the market has shifted since.

The valuation serves two purposes. First, the date-of-death value provides the dollar figure the Illinois probate court uses to verify the estate inventory. Second, the date-of-death value establishes the stepped-up tax basis that beneficiaries carry forward when they eventually sell the inherited property.

Without a documented professional appraisal in Central Illinois, beneficiaries may face unexpected capital gains taxes on appreciation that occurred before they ever owned the property.

To order a date-of-death appraisal in Champaign County, executors should take these steps in sequence. Gather the property’s legal description, deed, and most recent tax assessment records before contacting the appraiser — complete information at engagement shortens turnaround time.

Provide the exact date of death in writing so the appraiser can confirm the effective date before beginning the assignment. Confirm that the appraiser holds an active Illinois Certified Residential Appraiser or Certified General Appraiser license appropriate to the property type.

Request a full USPAP-compliant appraisal report — not a restricted report or desk review, both of which lack the supporting documentation courts and the IRS require.

Ask the appraiser to explain the comparable sale selection methodology in the report body so the value conclusion is defensible if challenged by a beneficiary or examiner.

Reviewing the home appraisal process FAQs before the first conversation with the appraiser helps executors ask the right questions and avoid miscommunications that delay report delivery.

An Illinois appraiser determines date-of-death value by identifying comparable sales that closed on or before the date the property owner died, then adjusting those sales to reflect differences between each comparable and the subject property.

The appraiser physically inspects the subject property, photographs the property’s condition, and documents everything observable on the valuation date — not today’s condition.

Comparable sale selection is the most consequential step in the analysis. The appraiser selects three to six closed sales of similar properties, ideally within a six-month window of the date of death and within a defined geographic radius around the subject.

For estate appraisals in Champaign County, appraisers draw on sales data from Champaign, Urbana, Savoy, and surrounding communities, depending on property type and market depth.

The appraiser adjusts each comparable sale upward or downward based on measurable differences in square footage, bedroom and bathroom count, lot size, condition, garage, basement finish, and other market-relevant features.

The home appraisal inspection process for a probate assignment follows the same physical scope as a standard appraisal — every room, every system, every observable condition factor enters the analysis.

Adjusted sale values are then reconciled into a single opinion of fair market value. Fair market value means the price a hypothetical informed buyer would pay a hypothetical informed seller in an arms-length transaction with neither party under compulsion.

The appraiser documents every step of that reasoning in the USPAP-compliant report so that a court, a beneficiary, or an IRS examiner can independently trace each conclusion back to market evidence.

Executors who want to understand what influences that final number should review the reasons appraisals come in low before the report is delivered — surprises are easier to manage when the executor understands the methodology in advance.

| Appraisal Component | What the Appraiser Does |

| Property inspection | Photographs and measures the property; notes condition on valuation date |

| Comparable sale selection | Identifies 3–6 closed sales on or before the date of death |

| Adjustment grid | Quantifies differences between each comparable and the subject property |

| Reconciliation | Weighs adjusted values to produce a single fair market value opinion |

| USPAP report | Documents methodology, comparable sales, appraiser credentials, and effective date |

Executors dealing with unusual properties — rural acreage, mixed-use buildings, or complex properties in Champaign — should discuss the assignment scope with Whitsitt & Associates before ordering, as atypical properties require expanded market searches and additional analysis time.

Illinois probate courts accept a full USPAP-compliant appraisal report prepared by a licensed Illinois appraiser who has no financial interest in the estate outcome. Under 755 ILCS 5/ Section 14-2, the representative must engage a competent, disinterested appraiser — meaning the appraiser cannot be a beneficiary, creditor, or party with any stake in the estate’s distribution.

A valid probate appraisal report must include the effective date tied to the date of death, the appraiser’s active Illinois license number and credential level, documentation of a physical property inspection, a sales comparison analysis with identified and adjusted comparable sales, and a clearly stated dollar opinion of fair market value.

Reports that omit any of these elements — particularly the physical inspection or the comparable sale grid — are routinely challenged by beneficiaries and rejected by court-appointed referees.

Under 755 ILCS 5/ Section 14-3, inventories and appraisals may be introduced as evidence in any suit by or against the representative, but the appraisal is not conclusive if other evidence shows the estate was worth more or less than the appraised value.

A well-supported report that documents methodology transparently is far harder to displace than a summary valuation with minimal backup.

Executors who want to understand what makes an appraisal defensible before ordering one can review Whitsitt’s guidance on fair property valuations.

The Champaign County probate division, operating under the Sixth Judicial Circuit of Illinois, follows the procedures established under 755 ILCS 5/ and accepts USPAP-formatted appraisal reports as the evidentiary standard for real property in estate inventories.

Executors managing estates with both residential and commercial property valuations in Illinois should confirm that the appraiser holds a Certified General license — that credential is required for non-residential assignments.

Missing a court filing because the appraisal isn’t ready costs the estate time and the executor’s credibility. Request your estate appraisal from Whitsitt & Associates now — Champaign County executors count on accurate valuations delivered on deadline.

For larger Illinois estates, the probate appraisal must meet IRS Form 706 documentation standards as well as state court requirements. Form 706 — the U.S. Estate and Generation-Skipping Transfer Tax Return — requires that every parcel of real estate be reported at its fair market value as of the date of death, supported by a qualified appraisal meeting Treasury Regulation standards.

The federal estate tax filing threshold for 2026 is $15 million per individual under current law. Illinois imposes its own separate estate tax on estates exceeding $4 million in 2026, using the same date-of-death valuation standard. Executors whose estates approach either threshold should discuss appraisal scope and timing with their probate attorney before ordering the report, because IRS-grade documentation requirements are more stringent than standard probate court expectations.

For estates that do require Form 706, the IRS expects a fully supported valuation report — not a restricted report or a summary.

The report must document comparable sales tied to the date of death, the appraiser’s qualifications and license number, the methodology used to derive the value, and the effective date.

Executors must submit the appraisal report alongside the return; the IRS does not accept value conclusions stated without supporting documentation. Understanding how appraisals interact with tax assessments helps executors anticipate where IRS examiners focus their scrutiny.

Under IRC Section 2032, executors may elect an alternate valuation date of six months after the date of death if that election reduces both the gross estate and the total estate and GST taxes owed.

This election is irrevocable once made on the originally filed Form 706, applies to all assets simultaneously, and cannot be applied selectively to reduce only the real estate value.

Executors considering this election should confirm the strategy with their probate attorney and tax advisor before instructing the appraiser, as the alternate valuation date affects both the comparable sale search window and the report’s effective date.

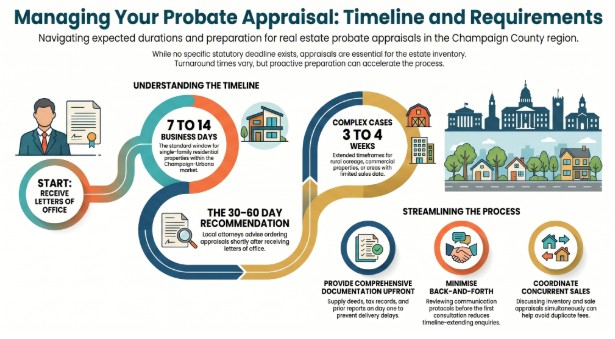

A probate appraisal in Champaign County typically takes seven to fourteen business days from inspection to delivery of the completed report. Standard single-family residential properties with adequate comparable sales data in the Champaign-Urbana market generally fall within that window.

More complex assignments — rural acreage, commercial properties in Champaign, or residential appraisals in Urbana with limited comparable sales — may require three to four weeks when the market search must extend further geographically or historically.

Turnaround time depends on property complexity, the appraiser’s workload at the time of the order, and the completeness of the information the executor provides at the time of engagement.

Executors who supply the deed, legal description, tax assessment records, and prior appraisal reports on the day they call generally receive faster delivery than those who provide documents piecemeal after the inspection.

Reviewing how to communicate effectively with your appraiser before the first conversation reduces the back-and-forth that extends timelines.

The Illinois Probate Act does not set a standalone statutory deadline for obtaining a real estate appraisal independent of the overall estate inventory.

However, most Champaign County probate attorneys advise ordering the appraisal within thirty to sixty days of receiving letters of office, because the estate cannot pay debts or distribute assets until the inventory is complete, and the inventory cannot be complete without the appraisal.

For estates where the property will be sold during the administration period, the appraisal process for buyers and estate sales follows different procedural steps than the inventory appraisal.

Executors managing a concurrent sale should discuss both assignments with Whitsitt & Associates simultaneously to coordinate inspection scheduling and avoid duplicate fees.

A residential probate appraisal in Champaign County typically ranges from $400 to $700 as of 2026 for a standard single-family property. Fees vary based on property type, size, location within the county, and the depth of historical analysis required by the retrospective effective date.

Properties where the date of death occurred 12 or more months before the appraisal order carry a modest fee premium because the appraiser must research and document historical market conditions rather than rely on current active listings.

Understanding the true value of an Illinois home requires more research when the effective date is in the past, and market conditions have shifted. Commercial properties and rural tracts are quoted individually based on scope and the availability of comparable sales.

The appraisal fee qualifies as a legitimate estate administration expense under 755 ILCS 5/ Section 14-2. The executor pays the fee from the estate account, along with attorney fees, court filing costs, and other administrative expenses — not from personal funds. Beneficiaries receive their distributions after all legitimate administration costs are satisfied.

Fee alone is a poor selection criterion. A poorly supported appraisal that triggers a beneficiary dispute, a probate court challenge, or an IRS audit costs the estate far more than the difference between a $450 report and a $650 one.

Choosing an appraiser with documented probate experience in Champaign County, a track record of the best local appraisal service, and court-accepted reports is the decision that protects the executor personally and the estate financially.

Reviewing common estate appraisal mistakes that Illinois executors make before selecting an appraiser helps avoid errors that can generate disputes after the fact.

Facing an estate deadline and not sure where to start? Whitsitt & Associates delivers court-accepted probate appraisals across Central Illinois — contact us today before the timeline gets tighter.

What is the difference between a probate appraisal and a regular home appraisal in Illinois?

A probate appraisal in Illinois establishes a property’s fair market value as of the date the owner died, not as of today’s market value. The effective date is fixed by law. A standard home appraisal uses the current date and serves lending, refinancing, or listing purposes. The methodology is similar, but historical research requirements differ.

Does every Illinois estate with real property need a professional appraisal?

Almost every Illinois estate with real property requires a professional appraisal. Illinois probate courts require licensed appraisals for real estate in the estate inventory whenever the estate exceeds $150,000 in 2026. Real property held in trust, joint tenancy, or under a transfer-on-death deed passes outside probate and may not require a court appraisal.

Can the executor hire any licensed appraiser in Illinois?

The executor may hire any licensed Illinois appraiser who is competent and disinterested under 755 ILCS 5/ Section 14-2. Disinterested means the appraiser cannot hold a financial interest in the estate’s outcome. For Champaign County probate, an appraiser with Central Illinois market experience produces more defensible comparable sale analysis than an out-of-market appraiser.

What happens if a beneficiary disagrees with the appraised value?

A beneficiary may introduce other evidence to challenge the appraised value, and Illinois courts may weigh that evidence under 755 ILCS 5/ Section 14-3. A USPAP-compliant report with documented comparable sales is substantially harder to displace than a summary valuation. Executors who choose a qualified local appraiser significantly reduce the risk of a successful challenge.

Does the executor need a separate appraisal for each property in the estate?

Yes. Each parcel of real estate in the estate requires its own independent appraisal with a dedicated comparable sale analysis tied to the same date-of-death effective date. Multiple properties ordered from the same appraiser at the same time may qualify for a reduced per-assignment fee — confirm this at engagement.

Can an executor order the probate appraisal before the court formally appoints them?

The appraiser can accept the engagement and schedule the inspection before letters of office are issued, but most executors wait for a formal appointment before authorizing estate expenditures. The appraisal report should list the date of death as the effective date. Most Champaign County probate attorneys advise completing the appraisal within thirty to sixty days after letters of office are issued.

What if the property was in disrepair on the date of death?

The appraiser documents the property’s condition on the valuation date and reflects that condition in the value conclusion. A property in disrepair on the date of death will appraise lower than a comparable maintained property. A below-market appraised value for a distressed property is legally required — the appraiser must reflect the actual condition, not the projected renovation value.

How does a probate appraisal affect the beneficiary’s capital gains taxes when they sell?

The date-of-death appraisal establishes the stepped-up cost basis that heirs carry into ownership of the inherited property. When a beneficiary later sells, capital gains tax applies only to appreciation above the appraised date-of-death value. Without a documented appraisal, the IRS may dispute the claimed basis, resulting in a larger taxable gain.

How do Illinois tax assessments compare to a probate appraisal value?

A county tax assessment and a probate appraisal serve different purposes and rarely produce the same number. Tax assessments are conducted by the county assessor’s office for property tax calculation and often lag current market conditions by an assessment cycle or more. A licensed appraisal determines fair market value as of a specific date using comparable sales and carries legal weight that an assessment does not.

What should an executor look for when selecting a probate appraiser in Champaign County?

An executor should confirm the appraiser holds an active Illinois Certified Residential or Certified General license, has documented experience with retrospective estate appraisals, and produces full USPAP-compliant reports. Asking for a sample report format and confirming the turnaround time before engaging protects the executor’s timeline and the quality of the estate’s documentation.