Originally published: June 2026

A date-of-death valuation in Illinois is a licensed appraiser’s written determination of a property’s fair market value as of the exact day the owner died.

Illinois executors must obtain this valuation before filing the estate inventory, distributing assets to beneficiaries, and closing the estate with the Champaign County probate court.

Illinois probate deadlines do not wait for grieving families to get organized. Schedule your date-of-death appraisal with Whitsitt & Associates in Champaign before the inventory deadline passes and the estate stalls.

A date-of-death valuation is a licensed appraiser’s retrospective determination of a property’s fair market value as of the exact day the property owner died. The effective date is fixed by law and cannot be changed by the executor, the appraiser, or the probate court after the fact. Whitsitt & Associates provides estate appraisal services in Illinois, specifically calibrated to this retrospective standard.

A date-of-death valuation differs from a standard current-market appraisal in one foundational respect: the appraiser does not assess the property’s value today.

The appraiser reconstructs what the property was worth on a specific past date using comparable sales that closed on or before that date, historical market data from that period, and a documented inspection of the property’s condition.

This backward-looking methodology is called a retrospective appraisal, and it requires an appraiser with documented experience searching historical market records — not simply pulling today’s active listings.

The valuation also differs from a real estate broker’s opinion, a comparative market analysis, or an automated online estimate. Illinois probate courts and the IRS treat those informal methods as legally insufficient documentation of estate value.

An executor who submits an online estimate or a real estate agent’s CMA as the basis for the estate inventory risks having the inventory rejected, triggering a court delay and potential personal liability for improper administration.

Understanding the full real estate appraisal process in Illinois before engaging an appraiser helps executors set accurate timelines and documentation expectations.

An Illinois executor must order a date-of-death valuation as soon as letters of office are issued by the probate court — and in most Champaign County estates, that means within the first two weeks of appointment, not the first two months.

The Illinois Probate Act of 1975 (755 ILCS 5/) imposes specific inventory deadlines that make early ordering essential, not optional.

Under supervised administration governed by 755 ILCS 5/ Article XIV, Section 14-1, the executor must file the estate inventory with the Champaign County probate court within 60 days of receiving letters of office.

A standard residential date-of-death appraisal in Central Illinois, as delivered by Whitsitt & Associates, takes seven to fourteen business days from inspection to report delivery. An executor who waits three weeks before ordering the appraisal leaves almost no buffer before the inventory filing deadline.

Executors who want to understand how the appraisal fits into the broader administration sequence should review the executor appraisal checklist before their first call with an appraiser.

Under independent administration — the more common structure in Champaign County — the executor must serve the inventory on the surety and all interested parties within 90 days of receiving letters of office, even though the inventory is not filed with the court.

The 90-day window sounds more generous, but executors who also need to arrange property access, locate the deed and legal description, and coordinate with beneficiaries often burn through it faster than expected.

The appraisal order itself should be placed within the first seven to ten days after letters of office are issued, regardless of administration type.

Ordering early creates buffer time for appraiser scheduling conflicts, extended market searches on retrospective assignments, and any corrections needed before the report is finalized.

| Administration Type | Inventory Deadline Under 755 ILCS 5/ | Recommended Appraisal Order Date |

| Supervised administration | 60 days after letters of office are issued | Within 7–10 days of letters of office |

| Independent administration | 90 days — served on surety and interested parties | Within 7–10 days of letters of office |

A date-of-death valuation becomes necessary beyond the probate inventory in several additional situations: when the estate includes real property subject to Illinois or federal estate tax, when inherited property will be sold, and beneficiaries need a documented stepped-up basis, or when a beneficiary dispute arises over the value of real estate in the estate distribution.

The Illinois estate tax applies to estates exceeding $4 million in 2026 under the Illinois Estate and Generation-Skipping Transfer Tax Act. The federal estate tax under IRS Form 706 applies to estates exceeding $15 million per individual in 2026.

The Illinois estate tax return and IRS Form 706 both require a fully supported USPAP-compliant appraisal report — not a summary valuation or a restricted report.

Executors managing estates near either threshold should discuss the appraisal scope and format with their probate attorney before ordering, as tax-grade documentation requirements are more detailed than those for standard inventory appraisals.

The stepped-up basis trigger is the one most executors overlook. Under IRS Publication 551 (Basis of Assets), when a beneficiary inherits real property, the tax basis of that property resets to its fair market value as of the date of death.

An asset is inherited with a basis equal to its date-of-death value — a stepped-up basis — because the basis is increased to reflect its value at the date of death, which reduces the capital gains taxes due upon the sale of an inherited asset.

A beneficiary who later sells the inherited property pays capital gains tax only on appreciation above the date-of-death value, not on the total sale price.

Without a documented professional appraisal in Central Illinois to establish the baseline, the IRS may dispute the claimed basis and assess taxes on a much larger gain.

The dispute trigger matters because Illinois courts allow competing evidence to challenge appraised values under 755 ILCS 5/ Section 14-3.

A well-supported appraisal with documented comparable sales and appraiser credentials is substantially harder to displace than an informal valuation. Executors who expect disagreement among beneficiaries over the property value should order the appraisal early and ensure the report meets the full USPAP standard.

An Illinois executor who delays ordering the date-of-death valuation risks four compounding consequences: missed inventory deadlines, stalled asset distributions, beneficiary disputes, and IRS documentation gaps that expose heirs to unexpected capital gains taxes years after the estate closes.

The first consequence is procedural. Executors of an estate have 60 days to catalog and account for all assets of an estate once they are appointed to the position of executor.

An executor who misses the inventory filing deadline under supervised administration must explain the delay to the Champaign County probate court. Courts in Illinois’s Sixth Judicial Circuit can impose sanctions on executors who demonstrate unreasonable delay in administering estate duties.

The executor’s personal credibility with the court — and with beneficiaries — depends on meeting these deadlines.

Every distribution to a beneficiary is blocked until the inventory is complete, the estate debts are identified and paid, and the court accepts the accounting. A delayed appraisal delays the inventory, which delays debt payment, which delays every distribution.

Beneficiaries awaiting inherited funds do not respond well to administrative delays, and such delays often escalate into formal beneficiary challenges that require attorney intervention.

Reviewing common estate appraisal mistakes that Illinois executors make helps identify the specific decision points where delays most often occur. The third consequence affects the estate’s tax position.

An executor managing a property sale during the administration period needs the date-of-death value to calculate the estate’s gain or loss on that sale for IRS Form 1041 — the estate’s income tax return.

Without a documented appraisal, the executor cannot accurately compute the taxable gain, creating IRS exposure that persists beyond the estate’s closing and can resurface years later when a beneficiary sells the property.

The fourth consequence is basis documentation. Beneficiaries who receive real estate without a documented date-of-death appraisal carry an undocumented stepped-up basis into their ownership.

When those beneficiaries eventually sell, the absence of an appraisal forces them to reconstruct the property’s value years after the fact — a more expensive and less defensible process than ordering the appraisal properly at the time of death.

Reviewing the retrospective appraisal process for probate in Illinois helps executors understand why contemporaneous ordering produces more defensible reports than late-ordered reconstructions.

Delays in the appraisal order cost the estate and the executor far more than the appraisal itself. Contact Whitsitt & Associates today to get the date-of-death appraisal ordered before the inventory deadline becomes a crisis.

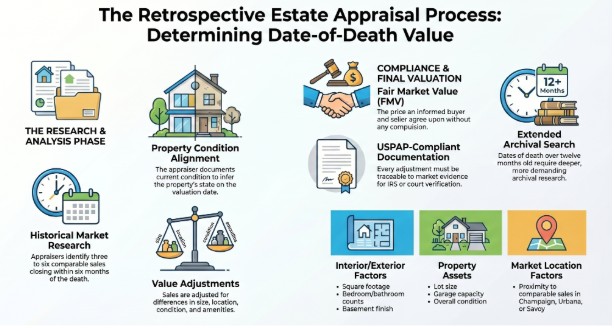

An Illinois appraiser establishes date-of-death value by researching comparable property sales that closed on or before the date the owner died, adjusting those sales for property-specific differences, and reconciling the adjusted values into a single fair market value opinion.

The appraiser performs a physical inspection of the subject property to document its condition on or near the valuation date, then cross-references that condition against historical market data.

Comparable sale selection drives the reliability of the retrospective analysis. The appraiser identifies three to six closed sales of similar properties in the subject’s market area, prioritizing sales that closed within a six-month window of the date of death.

For estate appraisals in Champaign County, the search typically covers Champaign, Urbana, Savoy, and surrounding communities, depending on property type and density of comparable sales.

When the date of death occurred more than twelve months before the appraisal order, the appraiser must research market conditions from that earlier period — a more demanding task that adds time and requires deeper archival market research.

The appraiser adjusts each comparable sale upward or downward to account for measurable differences between the comparable property and the subject: square footage, bedroom and bathroom counts, lot size, garage, basement finish, condition, and location.

Those adjusted values are then reconciled into a single opinion of fair market value. Fair market value means the price a hypothetical informed buyer would pay a hypothetical informed seller in an arms-length transaction with neither party under compulsion to buy or sell.

The home appraisal inspection process in Central Illinois for a retrospective estate assignment follows the same physical scope as a standard appraisal, with the additional requirement that observed conditions be cross-referenced against historical market data rather than today’s comps.

The appraiser documents all of this reasoning in a full USPAP-compliant report. Every comparable sale, every adjustment, and every value conclusion must be traceable back to documented market evidence so that the executor, the probate court, a beneficiary, or an IRS examiner can independently verify the methodology.

Executors dealing with unusual or high-value properties — rural farmland, multi-unit rentals, or complex properties in Champaign — should discuss the expanded scope of those assignments with Whitsitt & Associates before placing the order.

A date-of-death appraisal in Champaign County, as delivered by Whitsitt & Associates, takes 7 to 14 business days from property inspection to report delivery for standard single-family residential properties with adequate comparable sales data in the Champaign-Urbana market.

Properties requiring broader market searches — residential appraisals in Urbana with limited comparables, rural acreage, or commercial property valuations in Illinois — typically require three to four weeks.

Executors managing complex property assignments should place the appraisal order within the first seven days of receiving letters of office — not ten — to maintain a buffer within the 60-day supervised administration deadline.

Retrospective assignments in which the date of death is more than 12 months prior to the order require additional research time because the appraiser must locate and verify historical sale data rather than rely on current MLS records.

Executors who contact Whitsitt & Associates as soon as letters of office are issued — rather than after the inventory deadline is imminent — consistently receive reports with more time to review, correct, and submit before court filing requirements trigger.

Turnaround time also depends on how completely the executor provides property information at engagement.

Executors who supply the deed, legal description, most recent tax assessment, and any prior appraisal reports on the first call avoid follow-up delays that extend the already tight inventory window.

When do I need a date-of-death appraisal for probate in Illinois?

An Illinois executor needs a date-of-death appraisal as soon as letters of office are issued — ideally within seven to ten days of appointment. The inventory deadline under 755 ILCS 5/ runs 60 days for supervised administration and 90 days for independent administration. Waiting past the first week of the appointment removes all scheduling buffer.

What is the difference between a date-of-death valuation and a current appraisal?

A date-of-death valuation establishes a property’s fair market value as of the day the owner died, using comparable sales from that historical period. A current appraisal uses today’s market data and today’s effective date. Illinois probate courts and the IRS require the historical date-of-death value — a current appraisal does not satisfy either requirement.

Does a date-of-death valuation affect the beneficiary’s capital gains tax?

Yes. The date-of-death value establishes the stepped-up tax basis that beneficiaries carry into ownership under IRC Section 1014. When a beneficiary later sells the inherited property, capital gains tax applies only to appreciation above the date-of-death value. Without a documented appraisal, the IRS may dispute the basis and assess tax on a larger gain.

Can an executor use a Zillow estimate or a real estate agent’s CMA instead?

No. Illinois probate courts and the IRS do not accept automated valuation models or broker price opinions as valid documentation of estate value. The executor must provide a USPAP-compliant appraisal prepared by a licensed Illinois appraiser. Submitting an informal valuation risks inventory rejection, court delays, and exposure to an IRS audit.

What happens if the executor misses the inventory deadline?

An executor who misses the 60-day supervised inventory deadline must explain the delay to the Champaign County probate court. Courts may impose sanctions on executors who demonstrate unreasonable delay. Every asset distribution to beneficiaries remains blocked until the inventory is accepted — meaning a delayed appraisal stalls the entire estate administration sequence.

Does the date-of-death appraisal need to meet IRS standards if the estate is not taxable?

A full USPAP-compliant report is the correct standard for all Illinois probate appraisals, regardless of estate size. Estates below the Illinois $4 million and federal $15 million thresholds still benefit from a fully supported report because beneficiaries need documented stepped-up basis values, and courts may scrutinize the inventory if a beneficiary challenges the valuation.

How far back can a date-of-death appraisal go in Illinois?

Illinois imposes no statutory limit on how far back a retrospective appraisal can reach. Appraisers can establish date-of-death values for deaths that occurred years before the order date by researching archived market data. Reports ordered more than twelve months after the date of death take longer to complete and carry higher research costs, but remain valid and court-acceptable.

Who pays for the date-of-death appraisal in an Illinois estate?

The appraisal fee qualifies as a legitimate estate administration expense under 755 ILCS 5/ Section 14-2. The executor pays the fee from the estate account, along with attorney fees and court filing costs — not from personal funds. The estate’s legitimate administration costs are satisfied before assets are distributed to beneficiaries.

What if the property’s condition changed between the date of death and the inspection?

The appraiser documents the property’s current physical condition during the inspectio,n but calibrates the value conclusion to reflect conditions that existed on the date of death. Any significant changes — storm damage, repairs, demolition, or improvements made after death — must be disclosed to the appraiser at the time of engagement so the retrospective analysis accounts for them accurately.

Should the executor order a separate appraisal if the estate property will be sold?

Yes. The date-of-death appraisal establishes the inventory value and the stepped-up basis. A separate current-market appraisal may be appropriate if the executor plans to list the property during administration, as current market value and date-of-death value serve different purposes. Executors managing a concurrent sale should discuss both assignments with Whitsitt & Associates simultaneously.