Originally published: June 2026

Illinois probate courts require executors to file a verified inventory that includes the fair market value of every estate asset as of the date of death. A USPAP-compliant appraisal prepared by a licensed Illinois appraiser is the documentation standard that satisfies those court requirements for real estate and other significant property.

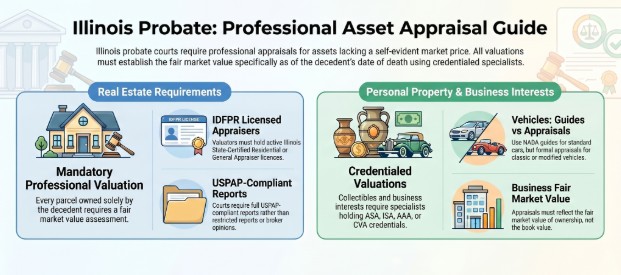

Real estate requires a licensed Illinois State-Certified Residential or General Appraiser. Personal property with material value requires a credentialed specialist.

Financial accounts and publicly traded securities do not require appraisals — date-of-death statements from the institution satisfy the inventory standard.

Illinois probate inventory deadlines arrive faster than most executors expect. Schedule your court-compliant appraisal with Whitsitt & Associates in Champaign before the 60-day window closes.

Illinois probate law requires every executor to compile and submit a complete, verified accounting of all estate assets valued as of the date of death — and to do so within tightly defined statutory deadlines. The Illinois Probate Act of 1975 governs this requirement across three sections of Article XIV.

Under 755 ILCS 5/ Article XIV, Section 14-1, the representative of a decedent’s estate must file in court a verified inventory of all real and personal estate that has come to the representative’s knowledge within 60 days after the issuance of letters of office.

The inventory must describe all real estate, including improvements and encumbrances on each parcel, state the amount of money on hand, and list all personal estate.

A supplemental inventory must be filed within 60 days if additional assets come to the representative’s knowledge after the initial filing. Whitsitt & Associates delivers estate appraisals in Champaign timed to meet this statutory deadline.

Under 755 ILCS 5/ Article XXVIII, Section 28-6, independent administration follows a different procedure: the independent representative must mail or deliver a copy of the inventory to each interested person no later than 30 days before filing the verified report required by Section 28-11.

The inventory is served on interested parties — not filed with the court on the same 60-day schedule — but the valuation standard is identical.

Under 755 ILCS 5/ Article XIV, Section 14-2, if the representative believes it is necessary for the proper administration of the estate to determine the value of any goods and chattels, the representative may appraise the assets directly or may employ one or more competent, disinterested appraisers and pay each of them reasonable compensation from estate funds.

The word “disinterested” is statutory — the appraiser cannot hold any financial stake in the estate outcome. Executors who want a complete overview of the appraisal obligation should review the executor appraisal checklist before engaging an appraiser. The estate settlement appraisal process at Whitsitt & Associates is structured to satisfy this statutory standard.

Under 755 ILCS 5/ Article XIV, Section 14-3, inventories and appraisals — and authenticated copies of them — may be introduced as evidence in any suit by or against the representative.

An appraisal is not conclusive, however, if other evidence shows the estate was worth or was sold in good faith for more or less than the appraised value.

A well-supported, USPAP-compliant report is far harder to displace under Section 14-3 than an informal or summary valuation.

Illinois probate courts require professional appraisals for any estate asset whose value is not self-evident from a market statement, account balance, or publicly recorded price. The type of appraiser required depends on the asset class.

Real property is the most common asset requiring a professional appraisal in an Illinois probate estate. Every parcel of real estate owned solely by the decedent must be valued at its fair market value as of the date of death.

The appraiser must hold an active Illinois State-Certified Residential Appraiser license for one-to-four-unit residential properties, or an Illinois State-Certified General Appraiser license for commercial, industrial, or mixed-use properties.

Licenses are issued and verified through the Illinois Department of Financial and Professional Regulation (IDFPR). A USPAP-compliant full appraisal report — not a restricted report or a broker opinion — is the accepted documentation standard for real property in the estate inventory.

Personal property with material value requires a written appraisal from a certified personal property appraiser. Jewelry, fine art, antiques, firearms, coins, and collectibles require appraisers holding recognized credentials from organizations such as the American Society of Appraisers (ASA), the International Society of Appraisers (ISA), or the American Association of Appraisers (AAA).

Vehicles are typically valued using established market guides — such as NADA or similar sources —but a formal appraisal is required for classic, modified, or high-value vehicles where guide values are insufficient.

A decedent’s ownership interest in a closely held business, partnership, or LLC requires a business valuation from a credentialed business valuator — typically a Certified Valuation Analyst (CVA) or Accredited Senior Appraiser (ASA) with a business valuation specialty.

The valuation must establish the fair market value of the interest as of the date of death, not the book value or the enterprise value.

Financial accounts — checking, savings, brokerage, and retirement accounts — do not require a licensed appraisal. The executor obtains date-of-death account statements directly from the financial institution.

Life insurance proceeds payable to the estate are valued at the policy’s face amount. Publicly traded securities are valued at the mean between the high and low trading prices on the date of death.

| Asset Type | Appraisal Required | License or Credential Needed |

| Residential real estate (1–4 units) | Yes — USPAP-compliant full report | IL State-Certified Residential Appraiser |

| Commercial/industrial real estate | Yes — USPAP-compliant full report | IL State-Certified General Appraiser |

| Personal property (jewelry, art, collectibles) | Yes — written certified appraisal | ASA, ISA, AAA, or equivalent credential |

| Closely held business interests | Yes — business valuation | CVA, ASA Business Valuation specialty |

| Classic or high-value vehicles | Yes — formal appraisal | Recognized vehicle appraiser |

| Bank and brokerage accounts | No — account statement | N/A |

| Publicly traded securities | No — high/low price average | N/A |

| Standard vehicles | No — published guide value | N/A |

An appraisal satisfies Illinois probate court standards when it meets four requirements: the appraiser is licensed and disinterested, the effective date matches the date of death, the report is USPAP-compliant, and the methodology is fully documented.

Section 14-2 of the Illinois Probate Act requires the appraiser to be both competent and disinterested. An appraiser who is a beneficiary, a creditor, or has any financial interest in the estate outcome does not qualify.

Illinois real estate appraisers must hold an active license through the IDFPR and must comply with USPAP as maintained by the Appraisal Foundation — the national standards governing all licensed appraisal disciplines. An appraiser who fails to meet the disinterested standard produces a report that courts may reject as biased, regardless of the report’s technical quality.

The appraisal’s effective date must match the exact date of death. An appraiser who uses today’s market conditions rather than the conditions that existed on the date of death produces a report that does not satisfy the probate inventory requirement.

The effective date drives the comparable sale search, the market condition adjustments, and the final value conclusion — and courts will reject reports where the effective date is inconsistent with the inventory filing.

Understanding the full real estate appraisal process in Illinois helps executors confirm the effective date standard before ordering.

A restricted appraisal report — the abbreviated format that omits much of the supporting analysis — does not satisfy probate court standards or IRS documentation requirements.

The executor needs a full USPAP-compliant report that includes the effective date, the appraiser’s license number and credential, a documented property inspection, a sales comparison analysis with identified and adjusted comparable sales, and a clearly stated fair market value opinion.

Reviewing what makes a fair property appraisal in Illinois helps executors evaluate a report before submitting it to the court.

Under Section 14-3, an appraisal in evidence is not conclusive if other evidence shows the estate was worth more or less than appraised. A report that documents every comparable sale, every adjustment, and every reasoning step is far harder to displace in a beneficiary challenge than one that simply states a value.

The Champaign County probate division, operating under the Sixth Judicial Circuit of Illinois, follows the evidentiary standard established by 755 ILCS 5/ Article XIV, and courts that review estate inventories can and do scrutinize the underlying support for the values reported.

The $150,000 small estate threshold determines whether formal probate — and therefore the court inventory appraisal requirement — applies at all. Under 755 ILCS 5/ Section 25-1, as amended by the 104th General Assembly effective in 2026, estates with personal property valued at $150,000 or less (excluding motor vehicles registered with the Illinois Secretary of State) may qualify for the small estate affidavit process, which does not require a court-supervised probate proceeding.

Executors managing estates below this threshold may not need to file a court inventory at all — and therefore may not face the formal appraisal requirement under Section 14-1.

However, a date-of-death appraisal remains advisable even for non-probate estates involving real property, because beneficiaries still need documented stepped-up tax basis values under IRC Section 1014, regardless of whether the estate goes through formal probate.

Any estate that includes real property solely in the decedent’s name and exceeds $150,000 in total probate asset value requires formal probate and a court-accepted inventory — which means a licensed appraisal for every parcel of real estate.

Executors uncertain about which threshold applies to their estate should review the home appraisals guide for Central Illinois before consulting their probate attorney. Understanding the threshold in advance prevents the common mistake of assuming a smaller estate bypasses all documentation requirements.

An estate that looks straightforward at first — a single-family home, a bank account, and a vehicle — can easily exceed $150,000 in 2026 real estate market conditions across Champaign County.

Executors who do not confirm the estate’s total value before assuming the small estate affidavit applies risk opening an informal process that the court later rejects.

Executors navigating the line between small estate and formal probate need accurate valuations before making that determination.

Contact Whitsitt & Associates for a Central Illinois estate appraisal that meets court standards, whether the estate ultimately proceeds through formal probate or not.

An inventory appraisal that fails to meet Illinois probate court standards produces compounding consequences: the court rejects or challenges the inventory, asset distributions to beneficiaries are delayed, and the executor faces potential personal liability for improper estate administration.

Illinois probate courts review estate inventories for completeness and legal sufficiency. An inventory that lists real estate values without a supporting licensed appraisal, or that relies on an online estimate, a CMA, or an informal written opinion, may be challenged by any interested party under Section 14-3.

The court can require a supplemental inventory supported by a compliant appraisal, extending the administration timeline and increasing attorney fees charged to the estate. Understanding the probate appraisal process in Illinois before submitting the inventory prevents these rejections.

Every distribution to a beneficiary depends on a complete, court-accepted inventory. A rejected or incomplete inventory stalls every downstream step: debt payment, estate tax filing, and final distribution.

Beneficiaries waiting for inherited funds quickly lose patience, and stalled distributions often escalate into formal beneficiary challenges that require attorney intervention and court hearings.

An executor who submits a defective inventory may face personal liability for breach of fiduciary duty if the estate suffers financial harm as a result — for example, if a beneficiary receives less than their correct share because a real estate value was understated.

Section 14-3 protects executors who obtain professionally supported appraisals by establishing a documented record of reasonable, good-faith valuation.

Executors who skip the licensed appraisal step remove that protection entirely. Reviewing common estate appraisal mistakes Illinois executors make before submitting the inventory identifies the specific errors most likely to trigger court scrutiny.

What appraisals does the Illinois probate court require for the estate inventory?

Illinois probate courts require a USPAP-compliant appraisal by a licensed Illinois appraiser for every parcel of real estate. Personal property with material value requires a written appraisal from a credentialed specialist. Financial accounts and publicly traded securities do not require appraisals — date-of-death statements from the institution suffice.

What is the deadline for filing the estate inventory under Illinois probate law?

Under 755 ILCS 5/ Article XIV, Section 14-1, the executor must file the verified inventory within 60 days of receiving letters of office under supervised administration. Under independent administration governed by 755 ILCS 5/ Article XXVIII, the executor must serve the inventory on all interested parties no later than 30 days before filing the verified report under Section 28-11.

Can the executor value estate real estate without a licensed appraiser in Illinois?

No. Illinois probate courts do not accept informal valuations, online estimates, or real estate agent opinions as documentation of estate value. Section 14-2 of the Illinois Probate Act requires the executor to employ a competent, disinterested appraiser for asset valuation. A licensed appraiser producing a USPAP-compliant report is the only documentation standard courts and the IRS accept.

What does “disinterested appraiser” mean under Illinois probate law?

A disinterested appraiser under 755 ILCS 5/ Section 14-2 is an appraiser who holds no financial interest in the estate outcome. The appraiser cannot be a beneficiary, a creditor of the estate, or a party with any stake in the distribution. An appraiser who fails to meet this standard produces a report that courts may reject as biased, regardless of the report’s technical quality.

What happens if a beneficiary challenges the appraised value in the estate inventory?

Under 755 ILCS 5/ Section 14-3, an appraisal introduced as evidence is not conclusive if other evidence shows the estate was worth more or less than appraised. A USPAP-compliant report with documented comparable sales and full methodology is far harder to displace than a summary valuation. Executors who retain a qualified, licensed appraiser with probate experience significantly reduce the risk of successful challenges.

Does the appraisal fee come out of the estate or the executor’s personal funds?

The appraisal fee is a legitimate estate administration expense under 755 ILCS 5/ Section 14-2, which explicitly authorizes the representative to pay each appraiser reasonable compensation for services rendered. The executor pays the fee from the estate account, along with attorney fees and court filing costs — not from personal funds.

Does an estate below $150,000 still need an appraisal in Illinois?

An estate with personal property at or below $150,000 in 2026 may qualify for the small estate affidavit under 755 ILCS 5/ Section 25-1, bypassing formal probate. However, a date-of-death appraisal remains advisable for any estate containing real property because beneficiaries still need documented stepped-up basis values for future capital gains purposes.

What license must a real estate appraiser hold to satisfy Illinois probate court standards?

A real estate appraiser must hold an active Illinois State-Certified Residential Appraiser license for one-to-four-unit residential properties, or an active Illinois State-Certified General Appraiser license for commercial or mixed-use properties. Both licenses are issued by the Illinois Department of Financial and Professional Regulation. Appraisals prepared by unlicensed or out-of-state appraisers without Illinois licensure are not court-acceptable.

Can the executor use the same appraisal for the estate inventory and IRS Form 706?

Yes, provided the appraisal meets USPAP standards and documents the methodology, comparable sales, and the appraiser’s credentials with sufficient detail. The IRS Form 706 documentation standard is more demanding than the baseline probate inventory requirement — executors managing estates near the $4 million Illinois or $15 million federal estate tax thresholds in 2026 should confirm the report format with their probate attorney before ordering.

What should the estate inventory include for real property beyond the appraised value?

Under 755 ILCS 5/ Section 14-1(b), the inventory must describe each parcel of real estate, including improvements on the property and any encumbrances — mortgages, liens, or easements — affecting the parcel. The appraised fair market value is reported alongside this legal description. An inventory that lists a value without the required property description does not satisfy the statutory requirements of Section 14-1.