A residential appraisal is an independent, USPAP-compliant opinion of your home’s market value for a specific property on a specific date, supported by verified local comparable sales.

If you’re refinancing, buying or selling with a lender, settling an estate, or dealing with a divorce. The fear is real. A number that doesn’t hold up can derail financing, trigger renegotiations, delay court timelines, or create conflict when everyone needs clarity.

Whitsitt & Associates has served Central Illinois since 1983, and we deliver lender-ready residential appraisal reports rooted in Champaign-area market evidence and explained in plain English, so you understand the value and the “why,” not just the conclusion.

To get started, request an appraisal online or call Whitsitt & Associates at (217) 356-7605 to confirm scope, fee, and scheduling.

USPAP-compliant. Champaign County comps. Lender-ready reports. Clear timelines and communication. Licensed appraisers

A residential appraisal is a documented, USPAP-compliant opinion of market value for a specific home on a specific date, supported by local comparable sales and objective analysis.

It is not a home inspection, not a repair report, and not a pricing “guess”. It is the valuation lenders, courts, and decision-makers rely on when the outcome matters.

| Service | Purpose | Who uses it | Typical cost | Accepted by lenders |

| Residential Appraisal | Establish an independent, defensible market value as of a specific date | Lenders, homeowners, attorneys, estates, courts | Usually several hundred dollars. varies by property and scope | Yes |

| CMA (Comparative Market Analysis) | Estimate a likely listing or offer range to guide pricing strategy | Real estate agents, buyers, sellers | Often $0 as part of agent services | No |

| AVM (Automated Valuation Model) | Provide a quick algorithm-based value estimate using public data | Consumers, some lenders use it as a screening tool | Often free online | Not typically, not for full underwriting |

| Home Inspection | Evaluate the condition and identify defects or safety issues | Buyers, sellers, homeowners | Usually several hundred dollars. varies by size and inspection type | No |

If a lender, court, or formal decision is involved, you generally need an appraisal. If you’re mainly trying to choose a smart listing price or offer strategy, a market analysis may be enough.

The difference comes down to defensibility. An appraisal is independent and report-based. A market analysis is strategy-focused and designed to guide a transaction.

| Situation | Choose this if you want the right tool fast |

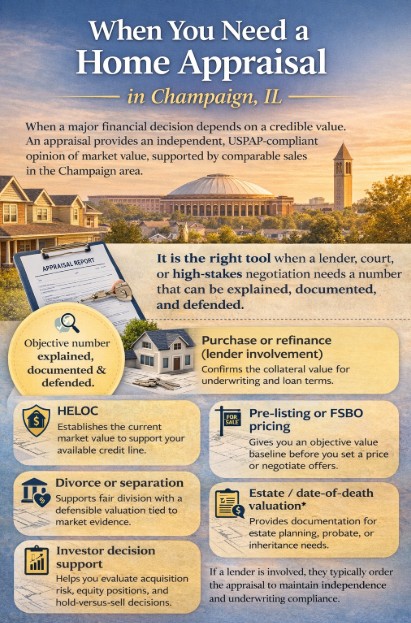

| Buying with a lender | Appraisal. The lender typically requires it and often orders it to confirm the collateral’s value. |

| Refinance | Appraisal. Your loan terms can depend on an independent opinion of the current market value. |

| Pre-listing confidence | CMA first for pricing strategy. Choose an appraisal if you want an independent value opinion before you list or anticipate disputes. |

| Divorce | Appraisal. You need a defensible value that can stand up in negotiation or court documentation. |

| Estate/probate | Appraisal. Useful for fair distribution and documentation. Retrospective or date-specific valuations may apply depending on need. |

| Private planning | Appraisal for a documented value you can rely on. Choose a CMA if you only need a rough pricing range for a potential sale. |

When a major financial decision depends on a credible value. An appraisal provides an independent, USPAP-compliant opinion of market value, supported by comparable sales in the Champaign area.

It is the right tool when a lender, court, or high-stakes negotiation needs a number that can be explained, documented, and defended.

If a lender is involved, they typically order the appraisal to maintain independence and underwriting compliance.

You should not have to wonder what happens next. Our process is straightforward, transparent, and built to reduce delays.

From the first call to the final report, we focus on accuracy, local market support, and clear communication. So you get a value conclusion you can actually use.

Schedule a Residential Appraisal in Champaign, IL Call (217) 356-7605 or use the form to request an appointment.

Most homeowners want two things right away. a clear schedule and no surprises.

We confirm the scope up front, schedule the inspection promptly, and complete the research and analysis required for a defensible, lender-ready report.

Turnaround depends on property complexity, local market activity, and how quickly we can verify the best comparable sales.

Appraised value is not based on a feeling or a headline estimate. It is supported by market data, verified comparable sales, and analysis that explains how the subject property competes in today’s Champaign County market. The strongest valuations are those that can be clearly tied back to real transactions and buyer behavior.

| Feature | What’s reviewed | How it’s supported |

| Kitchen and bath updates | Quality of finishes, age of remodel, functional improvements | Comparable sales with similar updates. paired sales where possible |

| Finished basement | Finish level, ceiling height, egress, usability, layout | Local comps with similar basement utility and finish quality |

| Garage | Size, attached vs detached, usability, condition | Comparable sales reflecting similar parking and storage utility |

| Lot size and usability | Corner lot, shape, drainage, privacy, outdoor function | Sales comparison to similar lots in the same micro-market |

| Deferred maintenance | Roof, HVAC, visible defects, safety issues | Market reaction shown in comps and condition adjustments |

| Additions and extra rooms | Permitted space, integration, quality, functional value | Comps with similar living area and functional utility |

| HOA factors, if applicable | Fees, restrictions, amenities, special assessments | Comps within the same HOA or similar HOA environments |

| Location influences | Busy roads, rail, commercial proximity, and views | Nearby comps demonstrating buyer reaction to similar influences |

Comparable sales are the backbone of a credible appraisal because they show what real buyers have recently paid for similar homes in the same market.

We prioritize the most relevant, verifiable sales first, then analyze differences in features and condition using market-supported adjustments so the final value conclusion is grounded in evidence, not assumptions.

We cannot “hit a number.” We report the value that the data supports.

Appraisal fees reflect the scope of work and the complexity of the assignment, not the value outcome.

A larger home, unusual layout, limited comparable sales, or a complex property type requires more research, verification, analysis, and documentation.

We confirm the scope and fee up front so you know what to expect before the inspection is scheduled.

| Appraisal type | Typical fee range | Notes |

| Standard single-family | Varies | Most common residential scope. Fee depends on size, complexity, and the availability of market data. |

| Condo/townhome | Varies | HOA factors, condo comps, and project characteristics can affect scope. |

| Multi-unit residential | Varies | More complex analysis and rent or income considerations may apply. |

| New construction | Varies | Requires additional verification of plans, specs, and limited sales support in some cases. |

| Rush options (if offered) | Varies | Subject to availability and scope. Confirmed case by case. |

The fastest way to lose time is to start with the wrong scope. That is when lenders request revisions, attorneys ask for more support, and timelines stretch as everyone waits for a report that aligns with the actual purpose.

Use the routes below to match your situation to the right appraisal from the start.

If you are unsure, tell us the property type and the purpose of the appraisal. We will point you to the correct scope before anything is scheduled.

When a value conclusion affects a loan approval, negotiation, or legal decision, you need an appraisal that is defensible and easy to understand, not a confusing report full of jargon.

Whitsitt & Associates has served Central Illinois since 1983, delivering USPAP-compliant valuations supported by Champaign-area comparable sales and communicated clearly, so you can move forward with confidence.

Learn more about the firm on About or Meet the Team. If you are ready to move forward, request an appraisal or contact Whitsitt & Associates to confirm scope and scheduling. You can also call (217) 356-7605.

Most residential inspections take about 30–60 minutes on site, depending on size, access, and complexity. Afterward, the appraiser verifies the data, researches comparable sales in the Champaign area, applies market-supported adjustments, and completes the written report. Delivery timing is confirmed when the assignment scope is set.

Fees vary by property type, size, complexity, and intended use. A typical single-family appraisal is usually several hundred dollars, but unique features, acreage, limited comps, or rush timing can increase the scope. We confirm the fee and expected turnaround before scheduling the inspection.

Ensure all areas are accessible, secure pets, and have utilities on. Provide a short list of upgrades and major repairs with approximate dates, plus HOA details if relevant. Cleanliness helps document condition, but value is driven by market evidence, not staging.

No. Upgrades support a higher value only when the local market shows that buyers are willing to pay more for similar improvements. Appraisers compare your home to recent sales and use market-supported adjustments. Project cost is not the same as value, and payback varies.

A low appraisal can be addressed. Options may include renegotiating the price, adjusting financing, increasing cash to close, or requesting a reconsideration if there are factual errors or better comps. Lenders control the review process, so documentation and evidence matter most.

Online estimates can provide a rough reference, but they are not a substitute for a USPAP-compliant appraisal. An appraisal includes an on-site inspection, verified data, and documented comparable sales analysis. For most loans, lenders rely on the appraisal report.

Yes, in most cases. Being present can help with access and questions about improvements, but the inspection is not a value discussion. If a lender ordered the appraisal, follow the lender’s access instructions. We focus on documenting features and conditions.

For most purchase and refinance loans, lenders order appraisals to maintain independence and compliance. Borrowers typically pay the fee through the loan process, but they generally do not choose the appraiser. This protects underwriting integrity and supports fair lending decisions.

Share information that helps verify characteristics and recent work. A simple upgrade list with dates, permits for major improvements, surveys or plats if available, and HOA documents for condos can be useful. Also note additions, finished areas, and recent roof or HVAC work.

When nearby comps are limited, the appraiser expands the search area and time frame while staying consistent with buyer behavior in Champaign County. More verification and support may be required for adjustments. That can increase complexity and sometimes extend turnaround.

A strong appraisal is peace of mind you can use. It gives you a clear, defensible value conclusion backed by comparable sales in the Champaign area, so you can move forward without second-guessing.

You get documentation that holds up with lenders and attorneys, fewer last-minute surprises, and a report written clearly enough that you understand the “why,” not just the number.

Outcomes you can expect

Request an Appraisal in Champaign, IL Call (217) 356-7605 or use the form to schedule your appraisal with Whitsitt & Associates.